Some costs are not 100% deductible for income tax and VAT. Depending on the business form, certain costs cannot be fully attributed to 'professional use'. For example, for 2021, a maximum of 50% of the VAT on car costs may be allocated to professional use, the remainder applies to private use.

While in the Netherlands the deductibility of costs is sometimes settled/corrected at the end of the financial year, the legislation in Belgium is stricter in this regard and states that this is processed accurately and correctly for every tax return.

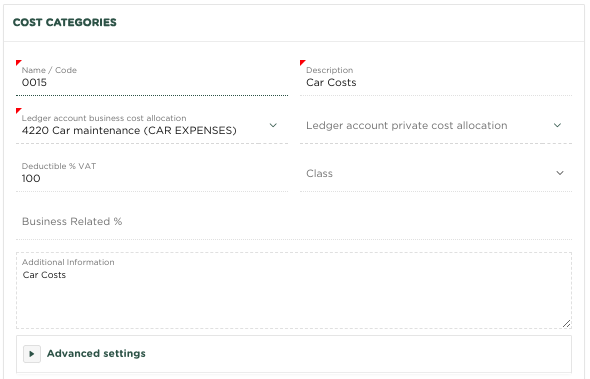

When entering Expenses (Purchases), it is therefore important that the correct Cost Category is used.

For each Cost Category it can be determined which percentage may be used for Income Tax (booking of professional costs and private related costs within the general ledger) and for the deductibility of VAT on certain costs.

The following example shows the deductibility (tax and VAT) for 'Car expenses'

If the costs of a repair to a passenger car are now entered, this Cost Category can now be used for correct processing within the general ledger and the VAT return. See the following example:

When entering an Expense for damage repairs to a passenger car, you now choose to post it to the Cost Category 'Car Costs'. After this Expense is made 'Final', it will be posted within the general ledger and processed within the VAT declaration.

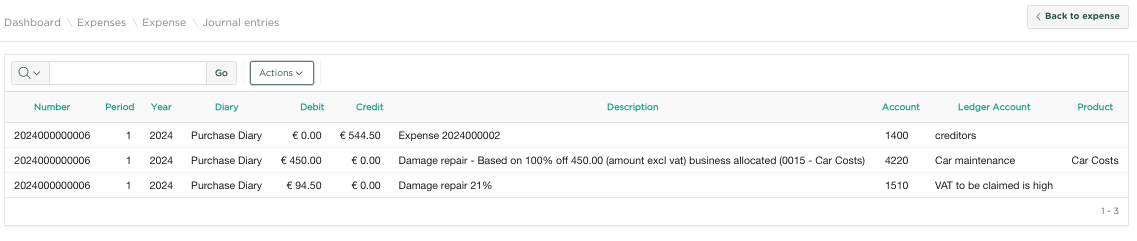

If we choose 'Journal entries' for the Expense, we see the following entries:

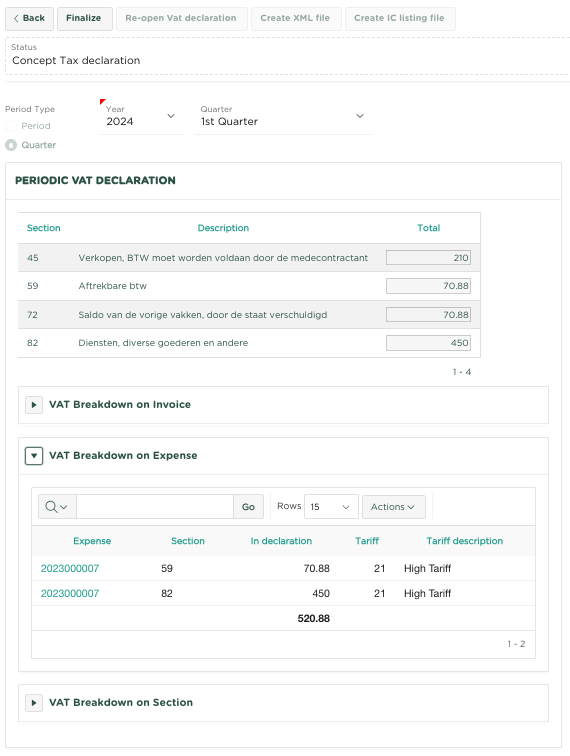

And if we choose the VAT declaration, we can see how the relevant Expense has been processed.

Voor sommige kosten geldt dat deze niet 100% aftrekbaar zijn voor inkomstenbelasting en Btw. Afhankelijk van de ondernemingsvorm, zijn bepaalde kosten niet volledig toe te rekenen aan 'beroepsgebruik'. Voor 2021 geldt bijvoorbeeld dat de Btw van Autokosten maximaal 50% mogen worden toegewezen aan beroepsgebruik, het restant geldt als privegebruik.

Waar in Nederland de aftrekbaarheid van kosten nog wel eens aan het eind van het boekjaar wordt verrekend/gecorrigeerd, is de wetgeving in België hier strikter in en stelt dat deze bij iedere aangifte accuraat en correct wordt verwerkt.

Bij het invoeren van Uitgaven (Inkoop) is het daarom belangrijk dat er gebruik wordt gemaakt van de juiste Kostencategorie.

Voor iedere Kostencategorie kan worden vastgelegd, welk percentage er mag worden gehanteerd voor Inkomstenbelasting (boeking van beroepskosten en privé gerelateerde kosten binnen het grootboek) en voor de aftrekbaarheid van de Btw op bepaalde kosten.

Het volgende voorbeeld toont de aftrekbaarheid (fiscaal en Btw) voor 'Autokosten'

Indien nu de kosten van een reparatie aan een personenwagen wordt ingevoerd, kan nu deze Kostencategorie worden gebruik voor de juiste verwerking binnen het grootboek en de Btw-aangifte. Zie het volgende voorbeeld:

Bij het invoeren van een Uitgave voor schadereparatie aan een personenwagen, wordt nu gekozen om deze te boeken op Kostencategorie 'Autokosten'. Nadat deze Uitgave 'Definitief' wordt gemaakt, zal deze worden geboekt binnen het grootboek en worden verwerkt binnen de Btw-aangifte.

Als we vanuit de Uitgave kiezen voor 'Journaalposten' zien we de volgende boekingen:

En kiezen we voor de Btw-aangifte, zien we op welke wijze de betreffende Uitgave is verwerkt.

| Info |

|---|

Related articles

| Content by Label | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

|

| Page properties | ||

|---|---|---|

| ||

|